Discover and read the best of Twitter Threads about #financialconditions

Most recents (7)

Thread🧵 on GMI's key macro charts by Raoul Pal. @RaoulGMI #GlobalMacro

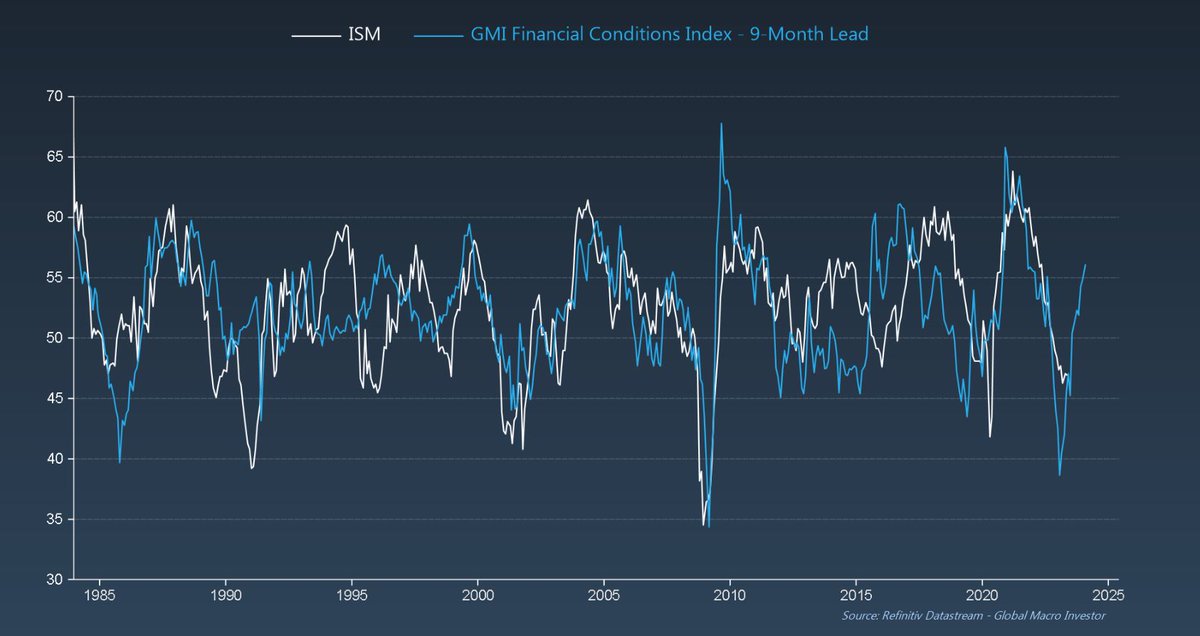

1/7 ISM is falling to 46.9, indicating short-term weakness. New orders point towards a drop closer to 45 in June. #GlobalEconomy

2/7 The GMI Financial Conditions Index suggests recovery, having already bottomed out and now rising. #FinancialConditions #EconomicTrends

As was widely expected, the @federalreserve’s Federal Open Market Committee raised the target range for the Federal Funds #policy rate by 50 basis points (bps), to between 0.75% and 1.0%, and announced the start of #runoff of the central bank’s balance sheet.

As previously suggested by the #Fed’s March minutes, the pace of runoff was confirmed today as $95 billion/month ($60 billion in U.S. #Treasuries and $35 billion in Agency #MBS, with a three-month phase-in period.

Also as expected, the statement reiterated that the #FOMC “anticipates that ongoing increases in the target range will be appropriate,” underscoring the seriousness of #Fed policymakers in getting #inflation and inflation expectations under control.

The Year 2021

Two 6 standard deviation moves so far.

- hedge fund deleveraging in the GameStop drama.

- relative value rates, sell-off in 5s vs rest of the curve, US treasuries.

*in both cases too much capital was hiding out in crowded venues.

Two 6 standard deviation moves so far.

- hedge fund deleveraging in the GameStop drama.

- relative value rates, sell-off in 5s vs rest of the curve, US treasuries.

*in both cases too much capital was hiding out in crowded venues.

When central banks do NOT allow the business cycle to function over longer and longer periods of time - the good news is wealth creation becomes colossal. Bad news is Capital moves into crowded venues, poised for disruption.

(2)

(2)

In rates, as the bond market sold-off. Originally, the long end 30s was deemed at risk, capital moved into 10s, 7s, a “safe” place. As selling pressure moved into the middle part of the curve, trillions moved into the front-end looking for duration risk shelter.

(3)

(3)

In January, core #CPI (excluding volatile food and energy components) came in at 0.2% month-over-month and 2.3% year-over-year. Over the year’s first half we expect Core #PCE to draw closer to 2%.

Yet, while we foresee continued firmness in #inflation, we’re skeptical it will be sustained and it won’t resemble demand-driven inflation, but rather it will be a function of favorable base-effects, #currency moves and a recovery in #commodity prices in the year’s back half.

From the standpoint of #monetary policy, we think the @federalreserve is on target with its policy stance today, and it will be closely watching the developments in inflation, in labor markets and critically in #financialconditions.

While #Fed Chair Powell’s testimony before #Congress didn’t produce any significant policy “news” that wasn’t already known, he was quite upbeat in his assessment of the U.S. #economy, even after being pressed on the possible impact of #coronavirus.

The Chair noted the recent strength of labor #markets and described the rate of #inflation as “low and stable,” acknowledging that it continued to run below the #FOMC’s symmetric objective of 2%.

We’ll be closely watching the #Fed’s language regarding “#financialconditions,” as this factor has become significantly easier in recent months and at some point, the Fed will likely engage with the possibility of reining in some of that #liquidity.

Clearly, #markets are in the midst of a #volatility spike, and indeed economic data for a time will be more #volatile and less certain, but at times like this it’s particularly important for investors to think hard about those factors that matter most to markets.

As such, next of our 8 @blackrock blog themes are: 3) that “1.8%” can still be a guidepost for understanding the trajectory of #economy and #markets in 2020, assuming #coronavirus risk can be mitigated; and 4) #inflation may see its best post-crisis year, but not exceed 2%.

More specifically, we think U.S. real #GDP growth and core #inflation are likely poised to stabilize near longer-run averages of roughly 1.8% this year, but clearly significant left-tail risks to global growth have increased.

With last week’s backup in #yields, the market is implying that the next three #Fedhikes are now near certainties.

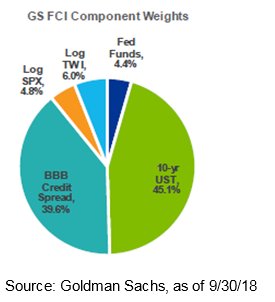

As such, the BBB corporate yield is now wider than the worst of the 2015-16 industrial recession, illustrating the impact of #Fedtightening on the cost of debt.

While broader #financialconditions are still some ways away from being prohibitive, given the strength of the #economy, corporate yields are effectively the biggest component - worth keeping an eye on.